इंटर गवर्नमेंटल पैनल ऑन क्लाइमेट चेंज (आईपीसीसी) की 2018 रिपोर्ट के अनुसार 2050 तक कोयला आधारित विद्युत उत्पादन लगभग बंद होना है। यह ग्लोबल वार्मिंग को दो डिग्री सेल्सियस के अंदर रखने के लिए आईपीसीसी द्वारा सुझाए गए महत्वपूर्ण उपायों में से एक है। इस तरह कोयला उद्योगों से राज्यों को होने वाली आय कम होती जाएगी। फिर खत्म होगी। भविष्य की इस चुनौती का हल, कोयला उत्पादक राज्य भावी नीतियों में तलाश रहे होंगे।

बचपन में कहावत सुनी, ‘अग्र सोची, सदा सुखी’। आज की दुनिया में जब टेक्नोलॉजी प्रेरित बदलाव बहुत तेज हों, तो इस जोखिम को कौन टाल सकता है? वैसे भी व्यावहारिक विजन के तहत इससे प्रभावित राज्यों की नीतियों में विकल्प की कोशिश होगी ही। पर क्या भविष्य के ऐसे सवाल, राज्यों की राजनीति में एजेंडा या मुद्दा हैं? क्या केंद्र के साथ मिलकर राज्य अपने-अपने प्रभावित होने वाले इलाकों की वैकल्पिक नीति व योजना बना रहे हैं? संबंधित राज्यों की राजनीति का यह लोक मुद्दा है? इसके समाधान के लिए लोक पहल है? मसलन झारखंड को सालाना बजट में कोयला से 5-6% आय होती है।

अगर यह क्रमशः घटे या बंद हो, तो सरकार को दूसरे स्रोत से वह आमद चाहिए। मुल्क में लगभग 3.5 लाख लोग कोयला उद्योग में प्रत्यक्ष रूप से जुड़े हैं। इन्हें रोजगार की जरूरत होगी। 1.5 करोड़ लोग अप्रत्यक्ष रूप से इस पर निर्भर हैं। इन्हें दूसरे क्षेत्र में अवसर देना होगा। झारखंड, बंगाल, उड़ीसा, छत्तीसगढ़, मध्यप्रदेश, आंध्रप्रदेश, तेलंगाना, महाराष्ट्र, तमिलनाडु वगैरह के सामने यह सवाल होगा।

एक और कारण है। भारत के बिजली उत्पादन में कोयला संचालित विद्युत उत्पादन का हिस्सा 71% के आसपास है। उधर सौर ऊर्जा उत्पादन लागत लगातार घट रही है। 2020 नवंबर में नेशनल थर्मल पावर कॉर्पोरेशन ने 470 मेगावाट सौर ऊर्जा प्लांट (सोलर पावर) की निविदा 2.01 रुपए प्रति किलोवाट पर पाई। यह लागत कीमत मौजूदा कोयला आधारित ऊर्जा से 40% कम है।

2015 में पर्यावरण, जंगल और मौसम परिवर्तन मंत्रालय ने कोयला आधारित ऊर्जा संयंत्रों के लिए नई प्रदूषण नीति तय की। तत्कालीन पावर प्लांट्स को, दिसंबर 2017 तक इसका पालन करना था। नए पावर प्लांटों को जनवरी 2017 के बाद, यह मापदंड लागू करना था। किसी भी कोयला पावर प्लांट ने यह मानक पूरा नहीं किया। यह समय सीमा बढ़ाकर 2022 हुई।

दुनिया के जो मुल्क कोयला उद्योग का विकल्प ढूंढ रहे हैं, वे खनन श्रमिकों के लिए नया क्षेत्र ढूंढ रहे हैं। यहां ढांचागत बदलाव की जरूरत होगी। व्यापक अर्थ में यह सामाजिक-आर्थिक बदलाव होगा। उद्योगों को नया रूप देना होगा। इन्फ्रास्ट्रक्चर और आधारभूत सामाजिक संरचना में निवेश बढ़ाना होगा। इस काम में डिस्ट्रिक्ट मिनरल्स फंड (डीएमएफ) की राशि उपयोग हो सकती है, वैकल्पिक आर्थिक ढांचा बनाने-विकसित करने में।

भविष्य में यह उद्योग परंपरागत स्वरूप में नहीं रहता, तो हर कोयला उत्पादक राज्य को अलग-अलग नीति बनानी होगी, क्योंकि कोयला खनन का 257 साल पुराना वाणिज्यिक कारोबार (1774 से) बदलेगा। एक मुकम्मल रोड मैप, अभी से ही बनाना होगा।

कुछ दिनों पहले छत्तीसगढ़ ने ‘रिन्यूएबल एनर्जी रोड मैप’ बनाया है। दरअसल देश के पूर्वी राज्यों की ताकत मिनिरल पावर (खनिज संपदा) रही है। यह परंपरागत संपदा, पुराने स्वरूप में नहीं रहनेवाली। देश के पूर्वी क्षेत्र या राज्य, इस चुनौती को अवसर के रूप में बदल सकते हैं। जैसे झारखंड में सौर ऊर्जा की बड़ी क्षमता है, क्योंकि राज्य को वर्ष में 300 दिन सौर ताप मिलता है।

भारत में जिला खनिज फाउंडेशन कोष में लगभग 45,000 करोड़ रु. हैं। हर साल करीब 6-7 हजार करोड़ रु. इस मद में आते हैं। इसमें कोयला व लिगनाइट का हिस्सा 41% है, जिसका 45% ही उपयोग हो रहा है। डीएमएफ के अलावा कोयला क्षेत्रों में कोल सेस भी एकत्रित होता है।

हर साल इस फंड में करीब 38,000 करोड़ जमा होते हैं। वर्तमान में इसका उपयोग जीएसटी भुगतान में हो रहा है, लेकिन 2022 के बाद यह कोयला क्षेत्रों के विकास के लिए उपलब्ध होगा। डीएमएफ व कोल सेस में उपलब्ध राशि का उपयोग संबंधित राज्यों में भविष्य में संरचनात्मक बदलाव की दृष्टि से होना चाहिए।

Two 5-year cycles currently drive the implementation of the Paris Agreement (PA): one of communicating national targets (“Nationally Determined Contributions” NDCs) and one of taking stock of global efforts. In order to complete the ambition mechanism of the PA, which is critical for its full operationalisation and the achievement of its objectives, another 5-year cycle, the “Glasgow Ambition Cycle” (GAC), aimed at ratcheting up the collective ambition of NDCs, has been proposed. It is gaining significant traction and appeal for adoption at COP 26 in Glasgow under negotiations on Common Time Frames (CTF, see Ambition Cycle on course to land in Glasgow). The GAC provides an elegant and non-controversial solution to the sticking options currently being negotiated, and is meant to start in 2025 when countries would be requested to:

communicate (at least) a 2035 NDC (‘with a time frame up to 2035’);

re-visit any NDCs communicated earlier to see whether, in light of changed circumstances, their ambition could be increased; and

repeat these two steps, ceteris paribus, every five years – thus in 2030 they would be: communicating a 2040 NDC and revisiting (inter alia) the 2035 NDC communicated five years earlier, and so forth.

As recently remarked by Marianne Karlsen (Chair of the UNFCCC/PA Subsidiary Body for Implementation): “Parties are increasingly realizing the importance of the issue [CTF] to the overall dynamics and well-functioning of the Paris Agreement. Of course, it is important to keep in mind that CTF is very much a political issue because establishing timeframes often involves parliaments and cabinets. So, this has to be something that politicians also need to get on the radar to work with.”[1]

This is why this OCP blog post takes a look at domestic considerations and demonstrates that the GAC is flexible enough to be accommodated and workable in three key Parties: India, China and the European Union.

India. India has a well-established revolving five-year electricity planning cycle consisting of Electric Power Surveys (EPS) and National Electricity Plans (NEP). The Surveys involve annual demand projections for the next ten years as well as long-term (‘perspective’) projections for 15- and 20-year time horizons. The Plans contain a detailed growth strategy, including investments in generation, transmission, and distribution, for the next five years and the roadmap for the subsequent five years.

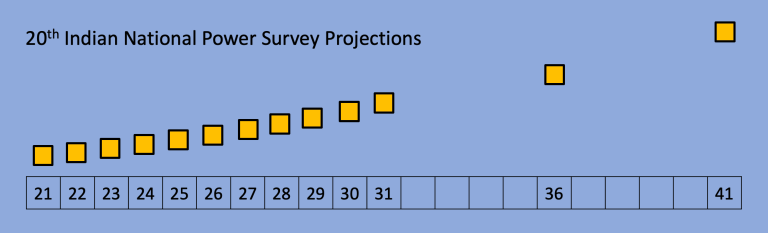

The 20th EPS, to be published in 2022, will contain yearly projections of electricity demand till 2030 and long-term projections for 2035 and 2040. The 4th NEP will be available in 2023; it will contain a detailed plan for 2022-27 and a perspective plan for 2027-32. As the electricity sector is the single largest source of GHG emissions in India, accounting for 47 per cent of the country’s total emissions, its planning cycle can be argued to be already in conformity with the GAC, and therefore in principle, the GAC can be accommodated in India’s NDC communication cycle, given the information in the 20th EPS/4th NEP.

China. China’s overall socio-economic development policy in the first half of the 21st century is dominated by two ‘Centenary Goals’; these mark the centenary of the Chinese Communist Party in 2021 and the centenary of the People’s Republic in 2049. As the mid-point between these two centenaries, 2035 has received special attention in China’s current policy making. The deliberations for the 14th Five-Year Plan (2021-25) include, for the first time, a longer-term vision with a 2035 target, which will set the development pathways for the next 15 years. This combination of short-term and long-term targets in China’s policy making is significant for global climate policy, not least because it is perfectly consistent with the proposed Glasgow Ambition Cycle.

The European Union. A key domestic consideration in the EU for determining the timeframe of climate targets is that implementing legislation can take up to 5 years to be adopted. The 2020 communication of a 2030 NDC update shows that a 2025 communication of a 2035 NDC should (in principle) be possible, even if a 2040 timeframe remains the preferred option among some of the key domestic constituents. Given that the Paris Agreement does not preclude the communication of multiple NDCs, there is no need to choose between the two options: the EU can communicate both a 2035 and a 2040 NDC in 2025, and thus take into account all domestic preferences and do so in a manner consistent with the Glasgow Ambition Cycle. The communication of a 2035 in order to facilitate a harmonisation of the GAC should not be seen as a mutually exclusive option, but rather a demonstration of political flexibility that will not prejudice the substantive essence of the EU’s overall ambition.

The Case of India: Electric Power Surveys and National Electricity Plans

India has an elaborate system for developing a National Electricity Plan every five years.[2] This system has been codified by an act of parliament – the Electricity Act of 2003 (‘the Act’). The Act obligates the Central Electricity Authority to formulate policies and plans for the development of the electricity sector, and to conduct and publish an Electric Power Survey (EPS) every five years to forecast both the country’s electricity demand and the contribution of various sources of electricity to meet that demand. The Act also stipulates the preparation of a National Electricity Plan (NEP) every five years, in accordance with India’s National Electricity Policy.

The EPS forecasts, every five years, the electricity demand for the entire country and for each State and Union Territory in the short, medium, and long term. Year-wise electricity demand projections are made for the next ten years, while long-term (perspective) demand projections are carried out for 15- and 20-year time horizons. So far, nineteen EPS have been published, the latest one in January 2017.

The 20th EPS will be published in 2022. It will contain:

Annual electricity demand projections for each State, Union Territory, Region, and All India in detail for the years 2021 to 2031 (see figure above);[3]

Electricity demand for the terminal years 2036 and 2041.

The NEP contains a five-year detailed plan and a 15-year perspective plan. It includes:

Short-term and long-term demand forecast for different regions;

Suggested areas/locations for capacity additions in generation and transmission, keeping in view the economics of generation and transmission, losses in the system, load centre requirements, grid stability, security of supply, quality of power (including voltage profile, etc.), and environmental considerations including rehabilitation and resettlement;

Integration of possible locations of capacity additions with the transmission system and development of the national grid – including the type of transmission systems and requirement of redundancies;

Different technologies available for efficient generation, transmission, and distribution; and,

Fuel choices based on economy, energy security, and environmental considerations.

The latest (Third) NEP was published in January 2018. It contains a review of the previous five-years (2012-17), a detailed plan for the next five years (2017-22), and a perspectives plan for 2022-27.

The Fourth National Electricity Plan will be available in 2023. It will contain a detailed plan for 2022-27 and a perspective plan for 2027-32.

From the above, it is clear that a revolving five-year planning cycle for the electricity sector is well-established in the country. As the electricity sector is the single largest source of GHG emissions in India (accounting for 47 per cent of the country’s total emissions, including LULUCF[4]), its planning cycle could become a basis for India’s NDC communication cycle.

The Case of China: Enhanced Five-Year Planning

At the 15th National Congress of the Chinese Communist Party (CCP) in 1997, President Jiang Zemin introduced two ‘Centenary Goals’ to guide the socio-economic development in China. The first goal refers to the centenary, in 2021, of the founding of the CCP, with the Centenary Goal of building a moderately prosperous society in all respects; the second one referring to the centenary, in 2049, of the founding of the People’s Republic of China, with the goal for China to become a basically modern socialist country.

At the 19th CPC National Congress in 2017, President Xi Jinping brought forward this goal to 2035 as a new mid-term goal, with the second Centenary Goal changing to China becoming fully modernized by 2050.

Three years later, in October 2020, President Xi Jinping introduced, for the first time, a longer-term vision – a 2035 development target – in the course of the discussions on the 14th Five-Year Plan (2021-25) at the 19th meeting of the CPC Central Committee.

This new combination of short-term and longer-term targets in China’ policy making is significant not only for China’s carbon emissions peaking and carbon-neutrality targets, but also for the international climate regime.

At the time of writing, some provinces, autonomous regions, and municipalities have published their 14th FYP and 2035 long-term policy recommendations. Among these, the important mid-

and long-term policy goals related to climate change include (but are not limited to): clarifying the carbon emissions peaking action plan, limiting coal use, increasing the share of renewable energy sources in the energy mix, promoting the intelligence and digitalization of energy development models, and developing green financial service systems. These targets will become the backbone of climate policy making at regional levels in the near future.

Since the formulation of its first five-year plan 70 years ago, China has completed thirteen FYPs, and FYPs will continue to provide guidance to the socio-economic development in China, despite debates on the effectiveness of such administrative economic planning. FYPs fit well with the proposed Glasgow Ambition Cycle, particularly in conjunction with the new longer-term 2035 planning horizon.

In short, the establishment of the 2035 target enables China to play an important role in international climate change negotiations. This is crucial for the ability of China’s own adaptive measures to engage with climate change impacts domestically, and also for the joint efforts of the international community to combat climate change. Combining the carbon emissions peaking and carbon-neutrality timelines, China has the opportunity to demonstrate its contribution to climate change mitigation and also its leadership, in the near future.

The Case of the EU: The Issue of Implementing Legislation

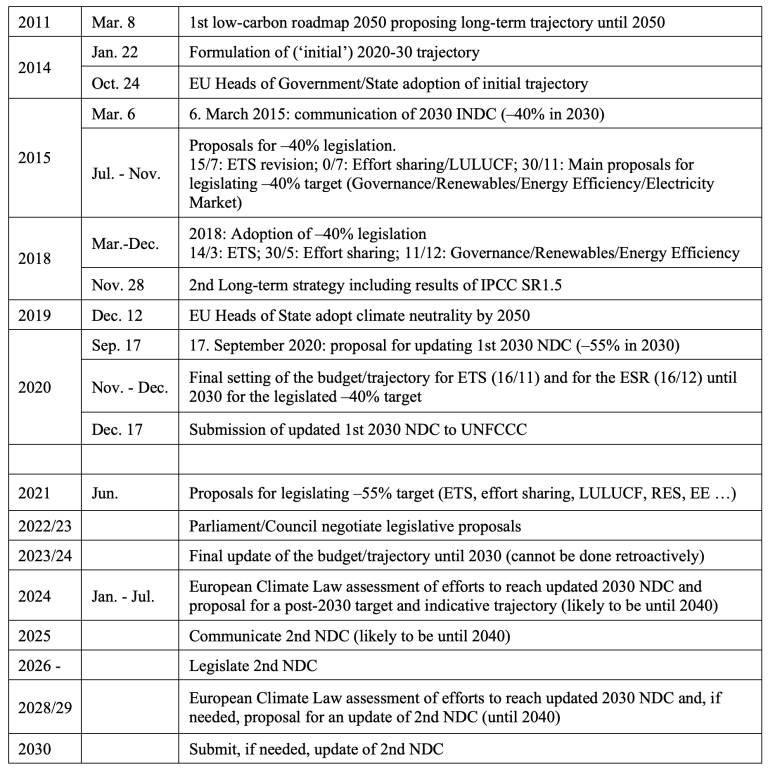

The Glasgow Ambition Cycle crucially requires the communication of a 2035 NDC by 2025. Could this be a realistic option for the EU? A practical way to assess possibilities is to look at precedents – in this case at EU past communications under the Paris Agreement (PA).

On 6 March 2015 (see Table 1 below), the EU communicated their Intended Nationally Determined Contribution (INDC) with a ‘point target’ of emissions in 2030 being at least 40 per cent below 1990 levels, which became its initial NDC on 5 October 2016, when the EU ratified the PA.

This was based on an EU-wide emission trajectory with annual figures from 2021 to 2030, formulated and adopted by EU heads of government in 2014. The subsequent formulation and adoption of the legislation required for implementing the 40 per cent target took almost five years, beginning in July 2015 and ending in December 2020 with the setting of the final 40 per cent target trajectory.

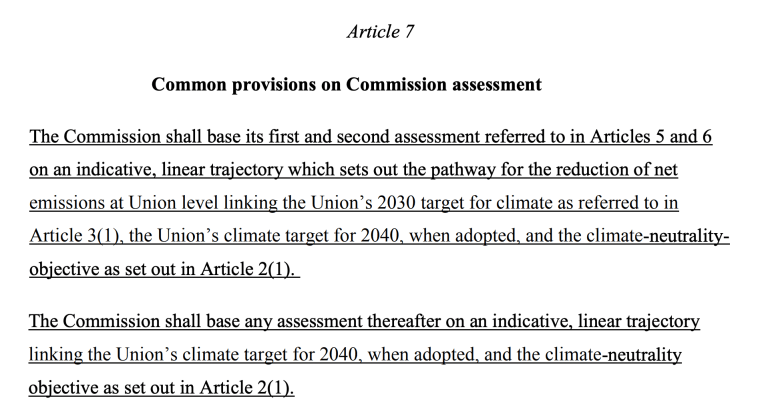

In March 2020, the Commission promulgated the European Climate Law [ECL], which not only mandates the EU to be ‘climate-neutral’ by 2050, but also “proposes the adoption of a 2030-2050 EU-wide trajectory for greenhouse gas emission reductions”[ECL], and five-yearly assessments of “the consistency of EU and national measures with the climate-neutrality objective and the 2030-2050 trajectory”[ECL], synchronized with the Global Stocktakes of the Paris Agreement.

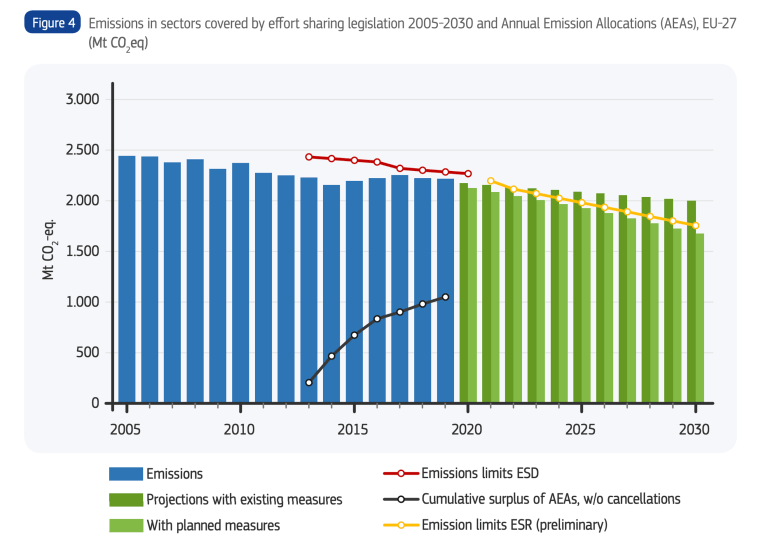

On 17 December 2020, the EU communicated an update of their initial NDC with a new, more ambitious target of at least 55 per cent below the 1990 level for 2030 emissions and – according to the EU Climate Action Progress Report, November 2020 (see also Figure 1) – the Commission is currently determining the annual emissions allocations (AEAs) for each country for the years 2021 – 2030, to take into account the updated, more ambitious, 2030 target.

Figure 1.Emissions in sectors covered by effort-sharing legislation 2005-2030 and Annual Emission Allocations (AEAs), EU-27 (Mt CO2 eq) [Fig. 4 in Climate Action Progress Report 2020]

What is to happen next? In a first instance, new implementing legislation for the 55 per cent target will have to be adopted, and it is expected that this will take (at least) until 2024, which means that in practice the implementation of the updated 55 per cent NDC is unlikely to commence before 2025.

Box 1. Draft by the European Council for the implementing regulation of the ECL (12 December 2020)

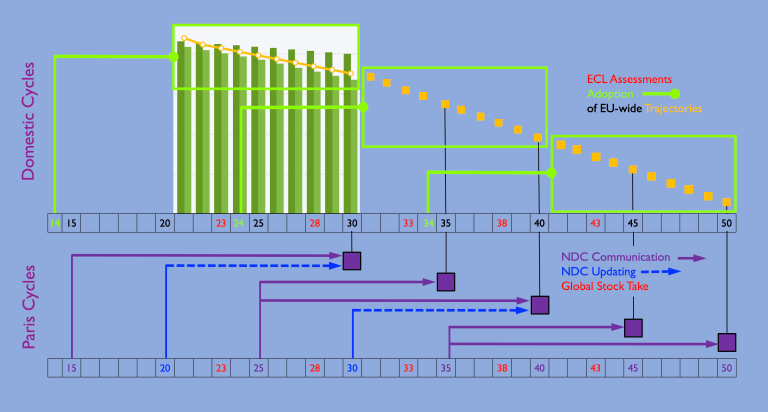

Assuming the adoption of the ECL by 2022, the next milestone will be the first of the ECL-mandated assessments in 2023. Following the pattern seen in the run up to the 2015 communication of the (I)NDC, it stands to reason – not least on the basis of the position of the European Council (see Box 1) – that this will be followed by the formulation and adoption of a second ten-year trajectory (2031-40, see Figure 2), presumably based on the 2050 net-zero trajectory mandated in the ECL.

Figure 2. EU Domestic and Paris Agreement Cycles

According to Art. 4.9 of the PA, all Parties have to communicate an NDC in 2025. The key question in the present context is about what timeframes the EU could realistically consider in light of domestic considerations?

One of the key domestic constraints, the time it takes to adopt the required implementing legislation (up to 5 years, as mentioned above), for one rules out another update of the 2030 NDC.

Given the INDC precedent, one option clearly is the communication of a 2040 NDC. But, to be sure, the 2020 communication of the updated 2030 NDC equally provides a precedent for the option of communicating a 2035 NDC, which seems to be the preferred option of a number of Member States,[5] and is consistent with the GAC. Fortunately, Art. 4.9 allows for multiple NDCs to be communicated simultaneously, so that there is no need to choose one over the other.

In short, keeping in mind the domestic legislative constraints, it is possible (as illustrated in Figure 2) for the EU to include the communication pattern set in Paris in a cycle that would be consistent with the GAC by communicating both a 2035 and a 2040 NDC in 2025, updating the 2040 NDC in 2030, and communicating a 2045 NDC and the 2050 (‘net-zero’) NDC in 2035.

Table 1. EU Climate Legislation/Regulation/NDC Timetable. Courtesy of Artur Runge-Metzger

The authors would like to acknowledge, with gratitude, feedback received (in alphabetical order) by Annika Christell, Kishan Kumarsingh, Geert Fremout, and Artur Runge-Metzger.

[1] Source: In conversation with SBI and SBSTA Chairs ERCST.

[2] References:

The Electricity Act, 2003 (available at http://www.cercind.gov.in/act-with-amendment.pdf).

19th Electric Power Survey, 2017 (available at https://cea.nic.in/wp-content/uploads/2020/04/summary_19th_eps.pdf).

National Electricity Plan, 2018 (available at https://cea.nic.in/wp-content/uploads/2020/04/nep_jan_2018.pdf).

[3] Note that strictly speaking, the projections are made for financial years, starting in April and ending in March of the following calendar year. However, to avoid cumbersome notation, the calendar year of the initial nine months is here used to designate the financial year in question, i.e., ‘2020’ instead of ‘FY 2020-21’.

[4] MoEFCC. (2018). India: Second Biennial Update Report to the United Nations Framework Convention on Climate Change. Ministry of Environment, Forest and Climate Change, Government of India.

[5] See Appendix 3 in Enhance Climate Ambition in 2020: Here’s looking at EU, kid!

The Government has introduced an amendment bill in the Lok Sabha on March 15, to further amend the Mines and Minerals (Development and Regulation) Act, 1957. Amendments have been proposed on a number of issues related to mining, including auctions, clearance and permit validity of mine leases, functioning of District Mineral Foundation (DMF) Trusts, among others. What comes across clearly from an overall reading of the MMDR Amendment Bill 2021, is that it increases the power of the Central Government in almost all aspects of decision-making on mining.

One of the most significant amendments in this regard is taking decisions on matters of DMFs. The Government had instituted DMF by amending the MMDR Act in 2015 to improve the social responsiveness of the mining sector. As specified in the law, the objective of DMF is to work for the interest and benefit of areas and people affected by mining and related activities.

The State Governments were entrusted with the primary responsibility of setting up DMFs in every mining district (of the respective state), through a notification. At the same time they were also vested with the power to prescribe the composition and functioning of DMFs.

The 2021 Bill proposes to increase the Centre’s say on matters of DMF. It has been specified that the “Central Government may give directions regarding composition and utilisation of fund” by the DMF.

The question is, what does this mean for DMF implementation, if the Bill becomes a law.

To answer this, it is important to consider what has been going on with DMFs in various states, and whether a direction from the Centre is necessary on its composition and functioning.

The MMDR Amendment Act 2015, under which DMF has been instituted, specifies that its composition and functioning, should be guided by three important people-centric laws. These include, the constitutional provisions as it relates to Fifth and Sixth Schedules (for governing tribal areas), provisions of the Panchayats (Extension to Scheduled Areas) Act (PESA), 1996, and the Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006 (in short the Forest Rights Act).

However, the DMF Rules as developed by most State Governments frustrates this. This has also been affecting DMF implementation.

First let us consider the composition of DMFs. Barring a handful, DMFs in most states/districts are dominated by officials and political members. This is true even for DMFs in Scheduled districts. There is negligible representation of Gram Sabha members, or general mining-affected people in the DMF body. This has resulted in top-down decision making. In most top mining districts, the affected community for whom DMFs have been developed, barely have any knowledge of it, or have any say about how it operates.

Second is the issue of DMF functioning and fund use. In nearly six years time, while more than Rs. 45,000 crores have accrued to DMFs across various districts in India, there is little perceptible change on ground with respect to development indicators, and basic factors of human well-being.

A major reason for this is lack of planning. Barely any DMF Trust has developed a DMF plan to use the funds in a targeted manner, and as per the need of the people who are the beneficiaries. This has led to ad-hoc decisions on fund use, without prioritizing issues where intervention is necessary. Just one example shows this clearly. While poverty and livelihood are critical issues for the mining-affected people, no substantial investment has happened. In the first five years, most districts have spent only 0-4% of the DMF budget towards this. Equally neglected areas have been child development, healthcare etc. in many districts. At the same time, there has been no significant effort for delineating the mining-affected areas, or identifying the mining-affected people.

The Centre’s intervention, which the 2021 Bill now suggests, presumably can help to improve DMF implementation, if the right directions are given. The Pradhan Mantri Khanij Kheshtra Kalyan Yojana (PMKKKY) guidelines must also be revised considering the current challenges with DMFs.

What is urgently required for the states, is to revise their DMF Rules. This is where the Centre can issue necessary directions. This can include directions on:

Revising the composition of DMF to include Gram Sabha members from directly mining-affected villages/panchayats (or ward members) in the DMF Governing Council. At least 10% of the members should be from directly affected villages (or wards if an urban area).

DMF planning, including preparation of annual action plans, and perspective plans, by engaging experts.

Identifying and notifying the beneficiaries (the mining-affected people) and delineating the mining-affected areas to improve effectiveness of fund use.

Setting up of DMF office in districts for purposes of coordination, planning, monitoring, and public disclosure of information. There is already 5% of DMF funds available for this.

Establishment of a state-level monitoring and co-ordination committee, for monitoring and co-ordination of DMF operations in various districts.

Improving accountability by information disclosure in public domain, and mandating both financial and performance audits of DMF Trusts.

The bottom line is, the Centre’s increase in power to intervene on DMF implementation, should not mean more top-down control. The directions must uphold the spirit of DMF, which is of a people-centric institution.

The private sector in India has traditionally avoided engagement on climate issues publicly. But this seems to be changing. On November 5, 2020, 24 leading companies signed a ‘declaration of the private sector on climate change’ to tackle the climate crisis. This is an important beginning as the private sector will have to play a crucial role in mobilising resources, knowledge, and innovation. And within the private sector, family-controlled conglomerates are uniquely positioned to lead the low/no-carbon growth trajectory.

Family ownership is the most dominant form of business around the world. Historically, family businesses have dominated the Indian industry. Until the 1990s, a few old business ‘houses’ were dominant, holding diversified business interests across the economy. Their dominance was partly enabled by the planned economy ‘license raj’ model of the time. Since the economic reforms of 1991, these older business houses have been challenged by new families and non-family entrants. But the power of family conglomerates as a business model has not diminished. While some of the older houses did not survive the reforms, many – such as the Tatas, the Bajajs, the Birlas, the Mahindras – did and flourished and are joined by new houses –the Ambanis, the Adanis, the Mittals, and the Jindals.

Presently, India has the third-highest number of publicly-listed, family-controlled companies in the world, after China and the United States. Fifteen of the BSE Sensex – the index of 30 reputed companies listed on the Bombay Stock Exchange – are family-controlled, accounting for more than half of the Sensex combined market capitalisation. Share-price returns of family businesses have also consistently outperformed non-family firms.

One of the key features of prominent family conglomerates in India is that they operate in fossil-fuel intensive sectors and are responsible for a significant share of India’s carbon dioxide emissions.

Today, just seven family conglomerates (Reliance, Adani, Tata, Aditya Birla, Mahindra, Jindal, and Vedanta) are responsible for emitting at least 530 million tonnes of CO2 annually. This is equivalent to 22% of India’s total CO2 emissions. In 2019-20, these seven groups operated 25% of India’s coal-based power plants (50,000 MW); produced 39% of India’s steel (43 million tonnes), 27% of India’s cement (91 million tonnes), and 22% of India’s passenger and commercial vehicles (0.92 million). They also accounted for 30% of oil refining capacity and 25% crude oil production.

If these companies get serious about climate action, India’s emission profile will look fundamentally different. While this ‘seriousness’ primarily comes down to the business argument, there is evidence that family businesses take a more long-term view on investments than non-family firms. Also, studies indicate that they are socially more responsible as they invest in the social and physical infrastructure of the areas they operate in.

The reason why a family conglomerate can take such investment decisions is its unique structure. Unlike other corporates, family businesses are organised around patriarchs/ matriarchs, who bear the ultimate responsibility and hold final decision-making powers. Though the ‘professionalisation’ of family businesses has resulted in hiring competent executives to advise and assist, they still run on the will of the founder or his appointed successor.

To avert a crisis like climate change, forward-thinking and long-term planning is required, for which the value of committed visionary leadership cannot be underestimated. As family conglomerates are organised around visionaries, if they sincerely act on the climate crisis, they can change the trajectory of their own business and that of the sector rapidly. To some extent, they already are doing so.

Mukesh Ambani has recently announced that Reliance Industries would become a net zero-carbon company by 2035. RIL is planning multi-billion dollar investments in hydrogen, wind, solar, fuel cells, and battery to become one of the world’s top “new energy” companies. Tata’s have also strongly signalled that they are moving out of the coal sector and moving into renewable energy, electric vehicles, and hydrogen-based steel making. Similarly, Mahindra has committed to aligning its operations with the science-based targets in the Paris Agreement, and Adani is investing hugely in the solar business to become the “world’s largest” green energy enterprise.

While these announcements and investments are encouraging, it is also a fact that many of these conglomerates continue to invest in fossil fuels. For example, during the recent auction of coal mines, Vedanta, Aditya Birla, Jindal, and Adani made acquisitions of coal assets, despite announcing ambitious renewable energy targets.

This seeming contradiction fits in with another well-known characteristic of Indian family conglomerates – they operate within a broad vision but have mostly grown opportunistically in areas where government incentives to expand are available. Therefore, even though they are bullish on a low-carbon future, much work needs to be done to move these family conglomerates from merely being followers of government policies to proactive climate champions. This can be a virtuous cycle – these conglomerates have a strong influence on government policy; if they are brought on board, a stronger climate policy is likely to follow.

Given their financial prowess and policy influence, the commitment of these families will be critical for accelerating the transformative changes that climate change requires. Cultivating their next generation to champion climate actions could be an important strategy to move them towards a green future. The business case will be an important part of the engagement, but not the only argument. These industry captains will have to be convinced of the new reality – our children are inheriting a dangerously climate-risked world. Family wealth will not provide infinite protection, but if used wisely, it can certainly contribute to making the world safer for everyone.